A safe withdrawal rate is the share of your portfolio you can spend in your first year of retirement, then raise with inflation each year, without running out of money. The textbook answer is the 4% rule. Withdraw 4% of your starting balance in year one, adjust the dollar amount for inflation each year after, and the money should last 30 years. On $1 million, that means $40,000 the first year, about $41,000 the next at 2.5% inflation, and so on.

We ran that rule through RetirFi's Monte Carlo engine, which models federal taxes on every withdrawal. Standing alone, 4% survived 64 of 100 simulated retirements. The number that rescues it for a typical retiree is not in the portfolio at all. It is Social Security.

The test: one retiree, $1 million, six withdrawal rates

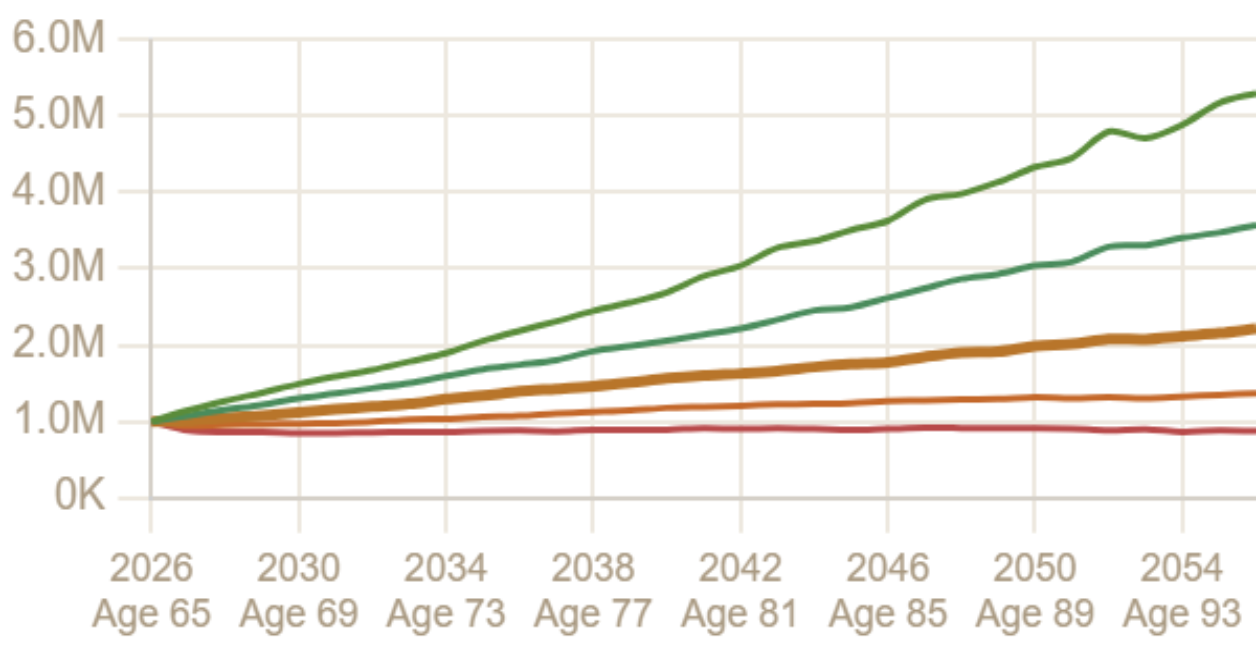

The test case is deliberately plain. A single 65-year-old retires today with $1 million and no income outside the portfolio. He holds $600,000 in a traditional 401(k) growing at 7%, $300,000 in a taxable brokerage at 6.5%, and $100,000 in cash at 4.5%. The plan runs to age 95, spending rises 2.5% a year with inflation, and the engine draws from taxable first, then cash, then the 401(k). The only dial we move is the withdrawal rate.

| First-year withdrawal | Rate | Success rate | Median depletion age, failed runs |

|---|---|---|---|

| $25,000 | 2.5% | 98% | 93 |

| $30,000 | 3.0% | 92% | 92 |

| $35,000 | 3.5% | 79% | 91 |

| $40,000 | 4.0% | 64% | 90 |

| $45,000 | 4.5% | 48% | 88 |

| $50,000 | 5.0% | 32% | 87 |

Each half-point of withdrawal rate costs between 6 and 16 points of success. At 4%, thirty-six of every hundred simulated retirements run dry, half of them by age 90. Rebuild the plan in the calculator at 1,000 simulations and you should land within a point or two of these numbers.

Why these numbers read lower than the textbook

The Trinity study puts a 4% withdrawal over 30 years above a 95% historical success rate. Our engine says 64%. Two modeling choices explain most of the gap, and both push in the conservative direction on purpose.

First, taxes. The academic studies treat every withdrawn dollar as spendable. In the simulation above, $600,000 sits in a traditional 401(k), so the engine grosses withdrawals up to cover federal income tax. Spending $40,000 costs the portfolio more than $40,000.

Second, volatility drag. The engine subtracts half the variance of each asset's returns from its expected return before drawing each year, which is how a 7% average return behaves once real-world volatility is applied to a shrinking balance.

Neither adjustment is pessimism about markets. Both are costs a real retiree pays that a frictionless backtest does not.

What actually makes 4% safe

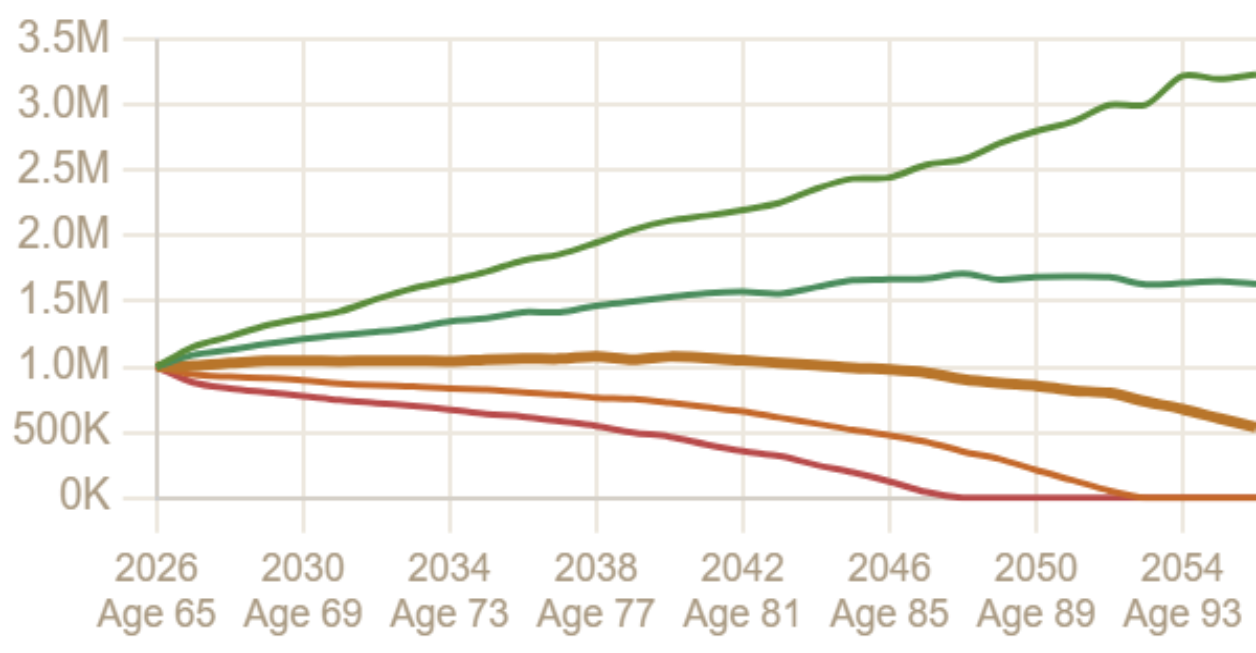

Give the same retiree an average Social Security check and the picture inverts. Add $2,000 a month claimed at 67, hold everything else fixed, and the 4% plan jumps from 64% to 100%. The median run now ends at age 95 with about $2.34 million, more than twice what he started with, and even the 10th-percentile run finishes with about $910,000.

The mechanics are simple. From 67 on, Social Security pays $24,000 of the $40,000 budget, so the portfolio only funds $16,000 a year. His true withdrawal rate is 1.6%, and the ladder above shows what the engine thinks of rates under 2%. The 4% rule holds up for typical retirees not because portfolios reliably support 4%, but because most retirees never actually withdraw 4% for long. Our guide to how long $1 million lasts in retirement runs the same retiree at three spending levels.

Where the rule came from

In 1994 financial planner William Bengen tested U.S. stock and bond returns back to 1926 and found the highest first-year withdrawal rate that survived every rolling 30-year retirement was about 4.15%. The 1998 Trinity study confirmed the result and gave the rounded-down "4% rule" its academic standing. Both are historical backtests of a frictionless portfolio, with no taxes, no fees, and no scenario worse than the past.

What withdrawal rate should you actually use?

The ladder above is one portfolio with no other income. Your situation moves the number, and the table below is a starting point, not a prescription. Retiring early stretches the horizon past the 30 years every figure on this page assumes; the 4% rule and early retirement covers that case.

| Situation | Suggested Rate |

|---|---|

| Retire at 65, 30-year horizon, flexible spending | 4.0–4.5% |

| Retire at 60, 35-year horizon | 3.5–4.0% |

| Early retirement (50s), 40+ year horizon | 3.0–3.5% |

| Very conservative, uncertain markets | 2.5–3.0% |

| Significant Social Security or pension income | Can be higher, SS covers base spending |

Look at the last row. If Social Security or a pension covers your essential spending, the portfolio only funds the gap, and its effective rate falls the way it did in the 100% run above. We walk through that math in how much do I need to retire. Flexible approaches such as guardrails, where you start near 5% and cut spending about 10% whenever the balance falls to a set floor, buy back much of the risk in the higher rows.

The bottom line

The 4% rule is a sizing tool, not a safety guarantee. On a portfolio with no other income, our tax-aware engine calls 4% a 64% plan and puts the comfortable rate closer to 3%. With an ordinary Social Security check, the same spending scores 100%. The rate that is safe for you depends on what share of your spending the portfolio must carry alone, and that is a number you can test directly with your own accounts, Social Security, and timeline.

Sources

- William P. Bengen, "Determining Withdrawal Rates Using Historical Data," Journal of Financial Planning, 1994.

- Philip L. Cooley, Carl M. Hubbard, and Daniel T. Walz, "Retirement Savings: Choosing a Withdrawal Rate That Is Sustainable," AAII Journal, 1998 (the Trinity study).

Find your actual safe withdrawal rate.

Enter your numbers and run a Monte Carlo simulation to see what withdrawal rate works for your specific timeline and assets.

Open the Calculator →